Medical Devices

US Bariatric Surgery Devices Market Analysis

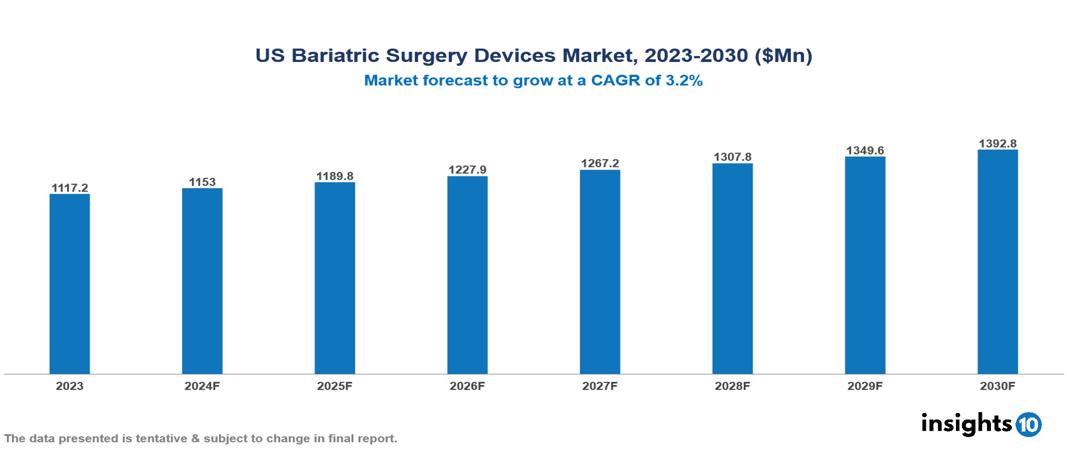

The US Bariatric Surgery Devices Marketwas valued at $1117.2 Mn in 2023 and is projected to grow at a CAGR of 3.2% from 2023 to 2023, to $1392.8 Mn by 2030. Major factors driving the market for bariatric surgical devices include the rising incidence of adult obesity brought on by altered lifestyle patterns and excessive calorie consumption. The demand for bariatric operations is also anticipated to rise over the forecast period due to increased government backing and growing public awareness of the market's unhealthy food and beverage offerings and how they affect BMI, thus driving the market growth of the Bariatric Surgery Devices. The prominent players in the market are Medtronic, Conmed Corporation, Johnson & Johnson among others.

Buy Now

US Bariatric Surgery Devices Market Executive Summary

The US Bariatric Surgery Devices Market is at around $1117.2 Mn in 2023 and is projected to reach $1392.8 Mn in 2030, exhibiting a CAGR of 3.2% during the forecast period 2023-2030.

Gastric bypass and other types of weight-loss surgery, also called bariatric or metabolic surgery, this involve making changes to your digestive system to help you lose weight. Bariatric surgery is done when diet and exercise haven't worked or when you have serious health problems because of your weight. Some weight-loss procedures limit how much you can eat. Others work by reducing the body's ability to absorb fat and calories. Some procedures do both. Bariatric surgery poses potential health risks, both in the short term and the long term. Bariatric surgery risks can include excessive bleeding, infection, reactions to anaesthesia, blood clots, lung or breathing problems etc. Longer-term risks and complications of weight-loss surgery vary depending on the type of surgery. they can include bowel obstruction, dumping syndrome, a condition that leads to diarrhoea, flushing, light-headedness, nausea or vomiting, gallstones, hernias, hypoglycaemia, malnutrition, ulcers etc.

According to Center for Disease Control and Prevention, in 2022, all U.S. states and territories had an obesity prevalence higher than 20% (more than 1 in 5 adults). Overall, the Midwest (35.8%) and South (35.6%) had the highest prevalence of obesity, followed by the Northeast (30.5%) and West (29.5%). DC had an obesity prevalence between 20% and less than 25%. Therefore, the market is driven by various factors such as rising incidence of obesity, technological advancements, rising awareness about bariatric surgery.

The prominent players in the market are Medtronic, B. Braun, Conmed Corporation, Johnson & Johnson among others.

Market Dynamics

Market Drivers

Rising obesity rates in US: US has been experiencing a steady increase in obesity rates over the past few decades. According Global Obesity Observatory in US, prevalence of obesity in 2022 was the 41.64%. This trend is likely to continue, creating a larger potential patient pool for bariatric surgeries and driving demand for related devices.

Increasing awareness of health risks associated with obesity: There's growing public awareness about the serious health complications linked to obesity, including type 2 diabetes, cardiovascular diseases, and certain cancers. This awareness is prompting more individuals to seek effective long-term weight loss solutions, including bariatric surgery.

Technological advancements in bariatric surgery devices: Ongoing innovations in surgical techniques and devices are making bariatric procedures safer, less invasive, and more effective. For example, the development of advanced laparoscopic and robotic-assisted surgical systems is improving surgical outcomes and reducing recovery times.

Market Restraints

High costs associated with bariatric surgeries and devices: Despite improvements in coverage, the high costs of bariatric procedures and devices is still a significant barrier for many patients. This is especially true for those without comprehensive insurance coverage or in provinces with limited public funding for these procedures.

Potential complications and risks of surgical procedures: Like any major surgery, bariatric procedures carry risks such as infection, bleeding, and adverse reactions to anaesthesia. Long-term complications like nutritional deficiencies and dumping syndrome can also occur. These risks may deter some patients from pursuing surgical options.

Limited availability of skilled bariatric surgeons: There's a shortage of surgeons specially trained in bariatric procedures in US, leading to long wait times in some regions. This shortage limits market growth and patient access to these treatments.

Regulatory Landscape and Reimbursement Scenario

Bariatric medical devices are regulated by Health US under the Medical Devices Regulations, which fall under the Food and Drugs Act. These devices are typically classified as Class III or IV, requiring stringent pre-market approval processes including safety and efficacy data submission. Manufacturers must maintain a certified Quality Management System and engage in post-market surveillance. The regulatory framework encompasses device classification, pre-market approval, quality management, post-market surveillance, and advertising regulations. Health US's Medical Devices Bureau oversees the entire process, ensuring devices meet safety, effectiveness, and quality standards before and after market entry.

Reimbursement for bariatric medical devices in US is complex and varies across provinces and territories due to the country's decentralized healthcare system. Generally, bariatric surgery is covered by provincial health insurance plans when deemed medically necessary, but coverage for specific devices can vary. Private insurance plans may offer additional coverage, but this varies by policy. Patients often face long wait times due to limited resources and high demand.

Competitive Landscape

Key Players

Here are some of the major key players in the US Bariatric Surgery Devices Market:

- Medtronic plc.

- Ethicon, Inc. (Johnson & Johnson)

- Olympus Corporation

- Apollo Endosurgery, Inc

- Intuitive Surgical, Inc

- ReShape Lifesciences, Inc

- Allurion Technologies, Inc

- EndoGastric Solutions, Inc

- GI Dynamics, Inc

- Mediflex Surgical Products

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

US Bariatric Surgery Devices Market Segmentation

By Products

- Minimally invasive surgical devices

- Stapling Devices

- Vessel-sealing devices

- Suturing devices

- Others

- Non-invasive surgical devices

By Procedure

- Sleeve gastrectomy

- Gastric bypass

- Revision bariatric surgery

- Non-invasive bariatric surgery

- Adjustable gastric banding

- Others

End Users

- Hospitals

- Ambulatory surgical centers

- Specialty Clinics

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Hong Kong Cardiac Monitoring Devices Market Analysis

Medical Devices

Europe Medical Devices Market Analysis

Medical Devices

Nigeria Medical Devices Market Analysis

Related reports (by geography)

Pharmaceuticals

US Cholesterol Therapeutics Market Analysis

Healthcare Services

US Connected Healthcare Market Analysis

Rare Diseases