Pharmaceuticals

Spain Cholesterol Therapeutics Market Analysis

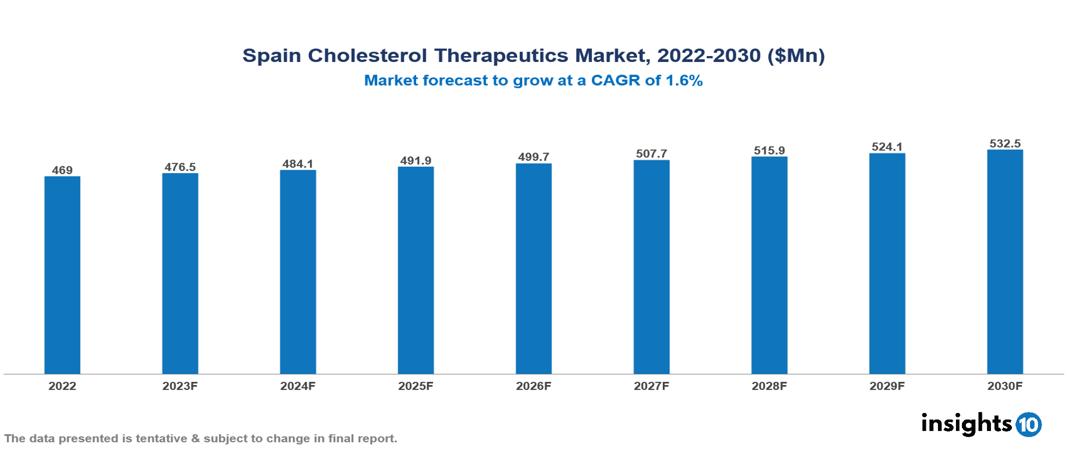

The Spain Cholesterol Therapeutics Market is anticipated to experience a growth from $469 Mn in 2022 to $532 Mn by 2030, with a CAGR of 1.6% during the forecast period of 2022-2030. The presence of prominent active pharmaceutical companies, coupled with the conducive environment fostered by ongoing research and therapeutic advancements, and the increased prevalence due to demographics and social factors further contribute to the dynamic growth of the market in Spain. The Spain Cholesterol Therapeutics Market encompasses various players across different segments such as Pfizer, Merck, Roche, Novartis, AstraZeneca, Johnson & Johnson, Almirall, Bayer, Grifol, PharmaMar, etc., among various others.

Buy Now

Spain Cholesterol Therapeutics Market Analysis Executive Summary

The Spain Cholesterol Therapeutics Market is anticipated to experience a growth from $469 Mn in 2022 to $532 Mn by 2030, with a CAGR of 1.6 % during the forecast period of 2022-2030.

Cholesterol is a fatty, waxy molecule that helps to form cell membranes and produce some hormones. While cholesterol is required for many basic activities, high amounts might pose health hazards. High cholesterol levels promote the buildup of plaque in arteries, resulting in atherosclerosis, which can lead to cardiovascular disorders such as heart attack and stroke. Several types of drugs try to control cholesterol levels. Statins, for example, reduce cholesterol synthesis in the liver. Other medications, such as bile acid sequestrants, function by binding to bile acids and limiting cholesterol absorption. PCSK9 inhibitors and fibrates are two other types that target various parts of cholesterol metabolism. These drugs are frequently administered with lifestyle improvements such as a nutritious diet and regular exercise. Ongoing research on the subject of cholesterol control focuses on generating new medicines and understanding the genetic elements that influence cholesterol regulation. Precision medicine advances attempt to match therapies to an individual's genetic profile, resulting in more tailored and effective interventions.

In the previous year, 40% - 50.5% of the adult population in Spain had hypercholesterolemia, totaling roughly 19.5 million people. Additionally, cardiovascular disease (CVD) is the major cause of mortality, accounting for 32% of all fatalities.

The presence of prominent active pharmaceutical companies, coupled with the conducive environment fostered by ongoing research and therapeutic advancements, and the increased prevalence due to demographics and social factors further contribute to the dynamic growth of the market in Spain.

Pfizer leads the Spanish cholesterol treatments market, with a market share of more than 20%, followed by Merck and Novartis. While big domestic firms such as Almirall are present in the landscape, their proportion is likely considerably less than that of multinational giants. Their percentage is higher only in the specific cholesterol drugs category, not the general market.

Market Dynamics

Market Growth Drivers

Increased Research & Development Investment: A notable surge in investment in R&D, particularly focusing on the development of Active Pharmaceutical Ingredients (APIs), is significantly driving market progress in the region. This heightened investment reflects a commitment to advancing pharmaceutical innovation, paving the way for the discovery and creation of more effective cholesterol-lowering drugs.

Advances in Novel Therapies: The market is being positively impacted by the introduction of therapies exhibiting promising efficacies and novel mechanisms of action. The anticipation surrounding the launch of new drugs with enhanced effectiveness is poised to be a pivotal driver in the cholesterol therapeutics sector. The emphasis on developing treatments with innovative mechanisms underscores the commitment to addressing hypercholesterolemia and related cardiovascular conditions more efficiently.

Higher Prevalence Rates: The high prevalence of hypercholesterolemia and cardiovascular diseases in Spain is a critical driver for the cholesterol therapeutics market. Given that cardiovascular diseases stand as the leading cause of mortality in the country, there is an escalating demand for advanced and effective cholesterol-lowering therapies. This demand is further intensified by the need to combat the rising incidence of hypercholesterolemia, reflecting a growing awareness of the importance of managing cholesterol levels for overall cardiovascular health.

Market Restraints

Reimbursement Issues: Limited reimbursement coverage stands out as a significant hindrance. The pharmaceutical landscape in Spain may not provide extensive reimbursement for cholesterol-lowering medications, impacting the financial viability of both patients and pharmaceutical companies. This limitation can deter market entry and affect the affordability and accessibility of cholesterol therapeutics, potentially slowing down the adoption of new medications.

Macroeconomic Issues: Economic and geopolitical considerations also play a role in restricting entry into the cholesterol market. Economic fluctuations, fiscal policies, and geopolitical tensions can influence market dynamics and create uncertainties. These factors may impact the purchasing power of consumers and the overall economic stability, affecting the pharmaceutical market's receptiveness to new cholesterol therapeutics.

Higher Treatment Costs: The higher cost associated with non-invasive technologies and instruments presents a challenge for pharmaceutical companies. Developing and introducing innovative non-invasive technologies for cholesterol management often involves substantial research and development costs. These elevated costs, coupled with the need for sophisticated instruments, can result in higher pricing for such technologies. In a market where cost considerations significantly influence healthcare decisions, the higher cost of non-invasive technologies becomes a barrier to entry, limiting the adoption of these advanced approaches.

Healthcare Policies and Regulatory Landscape

The Spanish Agency of Medicines and Medical Devices (AEMPS) regulates Spain's pharmaceutical and medical device sectors, which are critical to public health. As the nation's principal drug regulatory agency, AEMPS is responsible for guaranteeing the safety, effectiveness, and quality of drugs and medical devices on the market. It plays a critical role in the regulatory process, establishing stringent requirements for clinical trials and methodically tracking adverse responses. Its mandate includes assessing and approving innovative drugs based on scientific evidence of effectiveness and safety. The agency functions as a gatekeeper, ensuring that only pharmaceutical items that satisfy strict standards enter the Spanish market. Cost-effectiveness is a core pillar of Spain's healthcare policy, and AEMPS makes a substantial contribution to this goal by promoting the use of generic drugs. In essence, it not only protects the integrity of Spain's healthcare system, but it also acts as a driving force in responding to new medical breakthroughs and demographic trends.

Competitive Landscape

Key Players:

- Pfizer

- Merck

- Roche

- Novartis

- AstraZeneca

- Johnson & Johnson

- Almirall

- Bayer

- Grifol

- PharmaMar

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Spain Cholesterol Therapeutics Market Segmentation

By Indication

- Hypercholesterolemia

- Hyperlipidaemia

- Cardiovascular Diseases

- Others

By Drug Class

- Statins

- Bile Acid Sequestrants

- Lipoprotein Lipase Activators

- Fibrates

- Others

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End User

- Hospitals

- Speciality Clinics

- Homecare

- Academics & Research Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

China Endometriosis Drugs Market Analysis

Pharmaceuticals

Brazil Cough Remedies Market Analysis

Pharmaceuticals

UK Lung Cancer Drugs Market Analysis

Related reports (by geography)

Pharmaceuticals

Spain Constipation Therapeutics Market Analysis

Pharmaceuticals

Spain Alcohol Addiction Therapeutics Market Analysis

Healthcare Services

Spain Payer Service Market Analysis

Rare Diseases