OTC & Nutraceuticals

Italy Nutritional Supplements Market Analysis

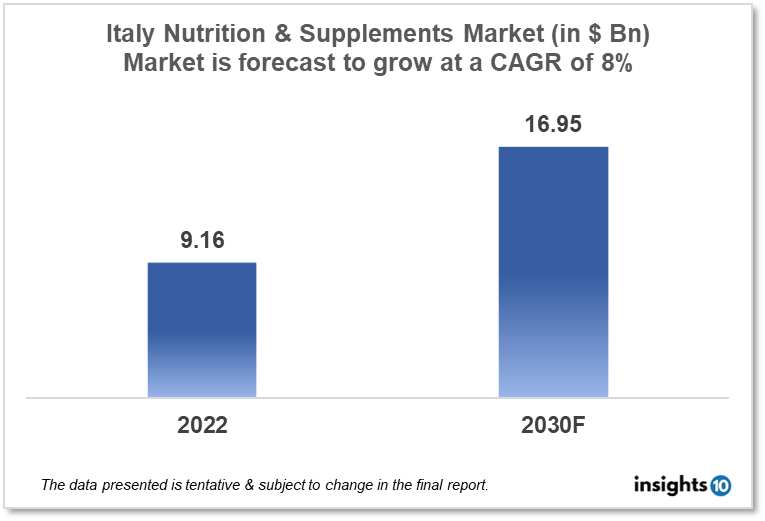

By 2030, it is anticipated that the Italy nutrition and supplements market will reach a value of $16.95 Bn from $9.16 Bn in 2022, growing at a CAGR of 8% during 2022-30. The market is primarily dominated by local players such as Solgar, Korashy, and Arkopharma. The market for nutrition and supplements in Italy is primarily driven by reimbursement scenarios, access to pharmacies, and strict government regulations. The Italy nutrition and supplements market in Italy is segmented by type, product, application, and distribution channel.

Buy Now

Italy Nutrition and Supplements Market Analysis Summary

By 2030, it is anticipated that the Italy Nutrition and Supplements market will reach a value of $16.95 Bn from $9.16 Bn in 2022, growing at a CAGR of 8% during 2022-30.

In Italy, 80% of people take dietary and nutritional supplements. Due to the widespread recognition of the value of a healthy diet and active lifestyle, Italy is a key geography for the nutrition and supplements market. The aging population of Italy is a major driver of this market, making it one of the largest in Europe and the world. In the upcoming years, the market for supplements will benefit from Italian consumers' growing understanding of the advantages of consumer goods made from natural ingredients (such as vitamins).

In 2020, it was projected that Italy would spend $4.89 Bn on nutritional supplements. Due to their expanded positioning beyond just supporting digestive health, including as immunity boosters and even mental health aids, probiotic supplements are expected to experience the fastest growth. The respiratory tract, musculoskeletal system, and gastrointestinal system were the three supplement categories with the largest sales growth between early 2021 and early 2022.

Market Dynamics

Market Growth Drivers

Since 2008, the value and volume of the Italy nutrition and supplements market have increased steadily, and the health-related issues during the COVID-19 pandemic have helped to further expand the market. Nearly 80% of food supplements were sold through pharmacies as of 2020, with the remaining 20% being sold by drugstores, big-box stores, and online. In Italy, female consumers account for a sizable portion of the market for food and health supplements.

Market Restraints

Reducing drug reimbursements and the ensuing search for substitute products may deter new players from entering the market.

Competitive Landscape

Key Players

- Solgar (ITA)

- Korashy (ITA)

- Arkopharma (ITA)

- Bios Line (ITA)

- Guaber (ITA)

- Aboca (ITA)

- Farmaderbe (ITA)

- Omega Pharma Italia (ITA)

- Pfizer

- GlaxoSmithKline

- Nestle

- Bayer

Recent Notable Update

December 2022: Sifi reports that EpiColin, a dietary supplement created especially for glaucoma sufferers, has officially launched in Italy. In the second half of 2022, Sifi will launch EpiColin, the third advancement in the treatment of glaucoma after Amiriox and Ecbirio, both of which are fully covered by the Italian NHS.

Healthcare Policies and Reimbursement Scenarios

The Italian Medicines Agency (AIFA) is the organization in charge of regulating dietary supplements in Italy. The items need to adhere to European Union (EU) rules for dietary supplements and have accurate labels that include details about the ingredients, recommended uses, and any applicable warnings. The Italian Advertising Self-Regulatory Code's rules must also be followed when running advertisements for dietary supplements.

In Italy, the National Health Service (Servizio Sanitario Nazionale) typically does not pay for dietary supplements. If a product is used to treat a particular condition and is prescribed by a doctor, it might be covered by insurance.

1. Executive Summary

1.1 Product Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Government Regulation in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel and Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

6. Methodology and Scope

Italy Nutritional Supplements Market Segmentation

By Product (Revenue, USD Billion):

- Sports Nutrition

- Sports Food

- Sports Drinks

- Sports Supplements

- Fat Burners

- Green Tea

- Fiber

- Protein

- Green Coffee

- Others (Turmeric, Ginseng, Cranberry, Garcinia Cambogia)?

- Dietary Supplements

- Vitamins

- Minerals

- Enzymes

- Amino Acids

- Conjugated Linoleic Acids

- Functional Foods

- Probiotics

- Omega-3

- Others

By Consumer Group (Revenue, USD Billion):

- Infant

- Children

- Adults

- Pregnant

- Geriatric

By Formulation (Revenue, USD Billion):

- Tablets

- Capsules

- Powder

- Softgels

- Liquid

- Others

By Delivery Channel (Revenue, USD Billion):

- Chemists/Pharmacists

- Direct-to-Consumer Sales

- E-commerce

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

OTC & Nutraceuticals

Latin America Nutritional Supplements Market Analysis

OTC & Nutraceuticals

Thailand Nutritional Supplements Market Analysis

OTC & Nutraceuticals

Hong Kong Over The Counter (OTC) Analgesics Market Analysis

Related reports (by geography)

Medical Devices

Italy Biomaterials in Healthcare Market Analysis

Healthcare Services