Medical Devices

US MRI Market Analysis

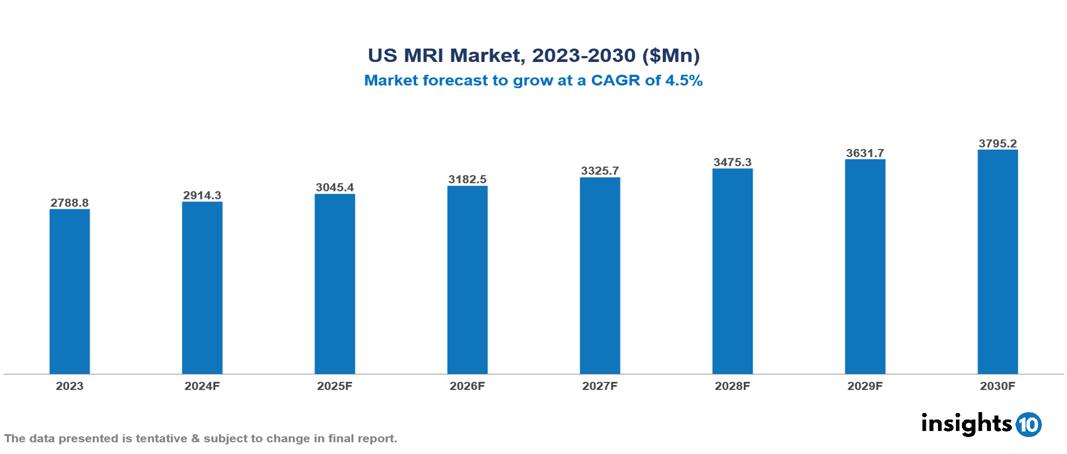

The US MRI Market was valued at $2788.80 Mn in 2023 and is predicted to grow at a CAGR of 4.5% from 2023 to 2030, to $3795.17 Mn by 2030. The key drivers of this industry include like increasing prevalence of chronic diseases, advancements in MRI, and medical tourism. The key players in the industry are Siemens Healthineers, Esaote North America, Rayus Radiology, and Fonar Corporation among others.

Buy Now

US MRI Market Executive Summary

The US MRI Market is at around $2788.80 Mn in 2023 and is projected to reach $3795.17 Mn in 2030, exhibiting a CAGR of 4.5% during the forecast period.

Magnetic resonance imaging (MRI) is a type of diagnostic test that can create detailed images of nearly every structure and organ inside the body. It uses strong magnetic fields and radio waves to produce detailed images of the inside of the body. The MRI machine is a large, cylindrical (tube-shaped) device that generates a powerful magnetic field around the patient and emits pulses of radio waves from a scanner. Some MRI machines resemble narrow tunnels, while others are more spacious. The intense magnetic field produced by the MRI scanner causes the atoms in your body to align in the same direction. Subsequently, radio waves are emitted from the MRI machine, which disrupt this alignment, causing the atoms to return to their original positions. As the radio waves cease, the atoms revert to their initial alignment and emit radio signals. These signals are then picked up by a computer, which transforms them into an image of the area being examined. This image is displayed on a viewing monitor.

Among member countries of the Organization of Economic Co-operation and Development (OECD), US has 37.99 units available per every million of its population. Therefore, the market is driven by significant factors like increasing prevalence of chronic diseases, advancements in MRI, and medical tourism. However, high cost, shortage of skilled professionals, and strict regulatory approval restrict the growth of the market.

The leading pharmaceutical companies include Siemens Healthineers and GE Healthcare for MRI machines. United Imaging Healthcare, Fonar Corporation, and Esaote North America are also significant contributors to the MRI market, with continuous research and development activities.

Market Dynamics

Market Growth Drivers

Rising Incidences of Chronic Diseases: The increasing prevalence of conditions like cancer and cardiovascular disease in US is driving the demand for MRI technology, which can aid in early detection and management of these diseases. This initiative is expected to improve the availability and accessibility of advanced medical technologies. The Centers for Disease Control and Prevention (CDC) states that over 795,000 people suffer from strokes annually in US, further contributing to the need for advanced MRI imaging.

Medical Tourism: US is a popular destination for medical tourism, with patients seeking high-quality imaging services like MRI scans. US healthcare system is at the forefront of medical imaging technology, with access to the latest generation of MRI machines, including high-field 3T and 7T systems. This advanced imaging equipment provides superior image quality and diagnostic capabilities. Compared to their home countries, international patients can often access MRI services in US more quickly, reducing the time they have to wait for critical diagnostic tests.

Technological Advancements: Innovations in MRI technology, such as the introduction of artificial intelligence-based software assistants and deep learning algorithms, are enhancing the capabilities and efficiency of MRI systems. AI-powered software can optimize MRI workflows by automating tasks like patient positioning, scan parameter selection, and image processing. These advancements, include faster scan times, improved image quality, and automated analysis.

Market Restraints

High Cost: The installation and maintenance of advanced high-field MRI machines like 3T and 7T systems is extremely costly in US. These systems require specialized facilities, extensive training for staff, and regular preventive maintenance to ensure optimal performance and patient safety. This makes it challenging for smaller healthcare facilities and private practices to invest in these advanced technologies, limiting their adoption across the US.

Regulatory Challenge: US FDA has implemented strict regulations for the import, installation, and operation of MRI machines to ensure patient safety and quality of care. It has established specific safety standards for MRI machines, including limits on the maximum magnetic field strength and noise levels that patients can be exposed to. These regulatory requirements can sometimes delay the adoption of new MRI technologies in the country.

Shortage of Skilled Professionals: US faces a shortage of qualified radiologists and MRI technicians, which is a key restraint for the growth of the MRI market. There is a shortage of trained radiologists in the US who can accurately interpret MRI images. This lack of specialized human resources can slow down the adoption and utilization of MRI technology in various regions of the country.

Regulatory Landscape and Reimbursement Scenario

The FDA's Center for Devices and Radiological Health (CDRH) is the primary regulatory body responsible for ensuring the safety and effectiveness of MRI systems in the US. The FDA regulates the manufacturing, repackaging, relabeling, and importation of MRI equipment. MRI machines are classified as Class II medical devices, which means they are subject to stricter regulations compared to lower-risk Class I devices. In addition to being medical devices, MRI systems are also considered radiation-emitting electronic products. Manufacturers must comply with the FDA's radiological health requirements under Title 21, Subchapter J, Parts 1000-1050 of the Code of Federal Regulations.

MRI procedures are reimbursed by Medicare under the Physician Fee Schedule (PFS) and the Outpatient Prospective Payment System (OPPS). Under the PFS, Medicare reimburses both the professional component (PC) and the technical component (TC) of MRI services.

Competitive Landscape

Key Players

Here are some of the major key players in the US MRI Market:

- GE Healthcare

- Siemens Healthineers

- Canon (Canon Medical Systems Corporation)

- Koninklijke Philips NV

- Neusoft Medical Systems

- Hitachi Medical Systems America

- Rayus Radiology

- Esaote North America

- United Imaging Healthcare

Toshiba Medical Systems

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

US MRI Market Segmentation

By Architecture

- Closed MRI Systems

- Open MRI Systems

By Field Strength

- Low Field MRI Systems

- High Field MRI Systems

- Ultra-High Field MRI Systems

By Application

- Neurology

- Musculoskeletal

- Cardiovascular

- Oncology

- Others ( Abdominal, Pediatric)

By End-User

- Hospitals and Clinics

- Diagnostic Imaging Centers

- Research Institutes

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Egypt Physiotherapy Equipment Market Analysis

Medical Devices

Poland Contraceptive Devices Market Analysis

Medical Devices

North America Pain Management Devices Market Analysis

Related reports (by geography)

Pharmaceuticals

US Obesity Drugs Market Analysis

Pharmaceuticals

US Cell Based Immunotherapy Market Analysis

Medical Devices

US ENT Devices Market Analysis

Pharmaceuticals