UAE LASIK Surgery Market Analysis

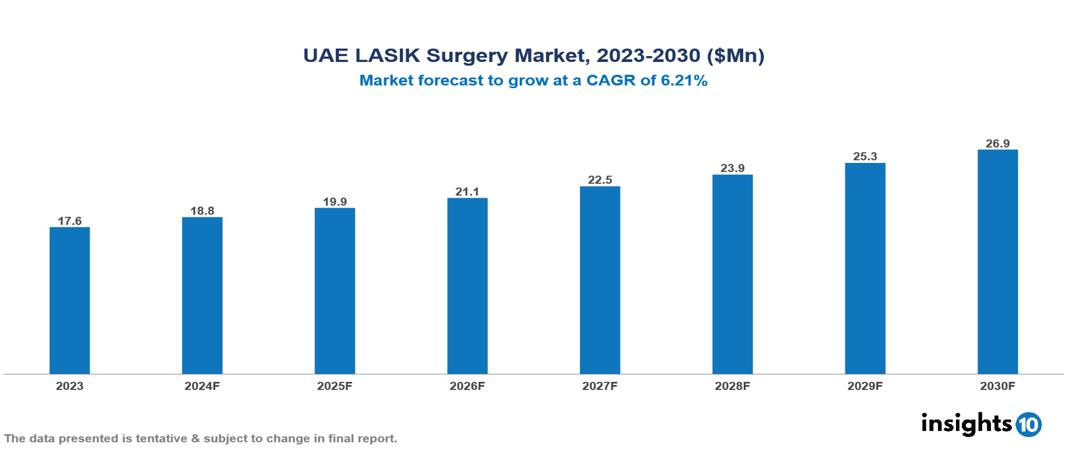

UAE LASIK Surgery Market was valued at $17.65 Mn in 2023 and is predicted to grow at a CAGR of 6.21% from 2023 to 2030, to $ 26.91 Mn by 2030. The key drivers of this industry include rising prevalence, high disposable income, and medical tourism destinations. The industry is primarily dominated by Johnson & Johnson Vision, Zeimer Ophthalmic System AG, Abbott, and Carl ZEISS AG, among others.

Buy Now

UAE LASIK Surgery Market Executive Summary

UAE LASIK Surgery Market was valued at $17.65 Mn in 2023 and is predicted to grow at a CAGR of 6.21% from 2023 to 2030, to $26.91 Mn by 2030.

LASIK, or laser-assisted in situ keratomileusis, is a popular refractive surgery that reshapes the cornea to correct vision problems like near sightedness, farsightedness, and astigmatism, significantly reducing dependence on eyeglasses or contact lenses. Before surgery, an ophthalmologist performs a comprehensive eye exam to determine candidacy. The outpatient procedure, lasting about 15-30 minutes per eye, involves creating a thin corneal flap with a microkeratome or femtosecond laser, reshaping the underlying corneal tissue with an excimer laser, and repositioning the flap without stitches. Post-surgery, patients may experience temporary discomfort and blurred vision, with risks including dry eyes, glare, halos, infection, and rare vision under or overcorrections.

In UAE, chronic diseases like cardiovascular diseases, diabetes, and chronic respiratory diseases cause around 55% of deaths, with cardiovascular diseases accounting for 34%. A study in Dubai revealed a high prevalence of dry eye disease at 62.6%, particularly among females and contact lens users, with high daily screen time and age as contributing factors. Visual impairment and blindness are estimated at 4.0% and 0.8% respectively, based on a hospital study in Al-Ain. Market is therefore driven by significant factors like rising prevalence, high disposable income, and medical tourism destination. However, high costs, limited public insurance coverage, and competition from alternative restrict the growth and potential of the market.

A prominent player in this field is Johnson & Johnson Vision, Zeimer which announced a collaboration with Schwind eye-tech-solutions to develop a new femtosecond laser platform for various ophthalmic applications, including LASIK surgery on June 2023. Other contributors include Abbott, and Carl ZEISS AG among others.

Market Dynamics

Market Growth Drivers

Rising Prevalence: UAE has a significant population with vision issues, with over 35% of adults suffering from myopia (near sightedness) according to a study in the Emirates Journal of Ophthalmology. This creates a substantial patient pool in need of corrective procedures like LASIK surgery, driving demand in the market.

High Disposable Income: UAE's high average disposable income, particularly among its citizens, enables more individuals to afford elective procedures like LASIK that enhance their quality of life. Additionally, there's a growing trend towards consumerism and investing in personal appearance and health, further fuelling the market.

Medical Tourism Destination: UAE is a renowned destination for medical tourism, attracting patients from neighbouring countries and beyond. This influx of international patients increases the overall volume of LASIK surgeries performed in the UAE, contributing significantly to market growth.

Market Restraints

High Cost of Surgery: Despite the UAE's high average income, the cost of LASIK surgery can still be a significant financial burden for some residents. Prices vary based on the surgeon's experience, the technology used, and the facility, making it less accessible for a broader population.

Limited Public Insurance Coverage: LASIK surgery is generally considered an elective procedure and is not typically covered by public health insurance plans in the UAE. This lack of coverage adds to the financial burden for patients, potentially deterring some from opting for the surgery.

Competition from Alternative: Availability of alternative vision correction methods like contact lenses and spectacle lenses poses competition to LASIK surgery. Patients might prefer these non-surgical options due to their lower upfront costs and the perceived safety of non-invasive treatments.

Regulatory Landscape and Reimbursement Scenario

UAE has a robust regulatory framework for LASIK surgery, managed by key governing bodies like the Department of Health (DoH) in each emirate, the Dubai Health Authority (DHA), and the Health Regulation & Licensing Department (HRLD). These bodies set stringent standards for medical facilities, license healthcare professionals, and ensure compliance with national healthcare regulations. They mandate strict pre-operative assessments, use of approved medical devices, informed consent procedures, and standardized post-operative care to ensure patient safety and optimal outcomes.

Regarding reimbursement, LASIK surgery is generally considered an elective procedure and is not typically covered by government-funded health insurance plans like Thiqa and Esaad, except in rare cases with severe vision problems. Some private health insurance plans offer partial coverage, but many patients in the UAE pay for LASIK surgery out-of-pocket. Costs vary based on factors such as the surgeon's experience, technology used, and the facility, with some clinics offering financing options to help manage expenses.

Competitive Landscape

Key Players

Here are some of the major key players in the UAE LASIK Surgery

- Schwind eye-tech-solutions

- Abbott

- Technolas Perfect Vision GMBH

- Johnson and Johnson Private Ltd

- Zeimer Ophthalmic System AG

- Alcon Inc.

- Laser Sight Technologies, Inc

- Bausch + Lomb Incorporate

- Carl ZEISS AG

- Nidek Co, Ltd

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

UAE LASIK Surgery Market Segmentation

By Type

- Wavefront Optimized

- Wavefront-Guided

- Topography Guided

- All Laser

By Vision Error

- Myopia

- Hyperopia

- Astigmatism

- Others

By Product

- Excimer Laser

- Femtosecond Laser

By End-User

- Hospitals

- Eye Care Clinic

- LASIK Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Poland Acne Drugs Market Analysis

Turkey Dermatological Therapeutics Market Analysis

Global Antifungal Drugs Market Analysis

Related reports (by geography)

UAE Cancer Immunotherapy Market Analysis