Pharmaceuticals

Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market Analysis

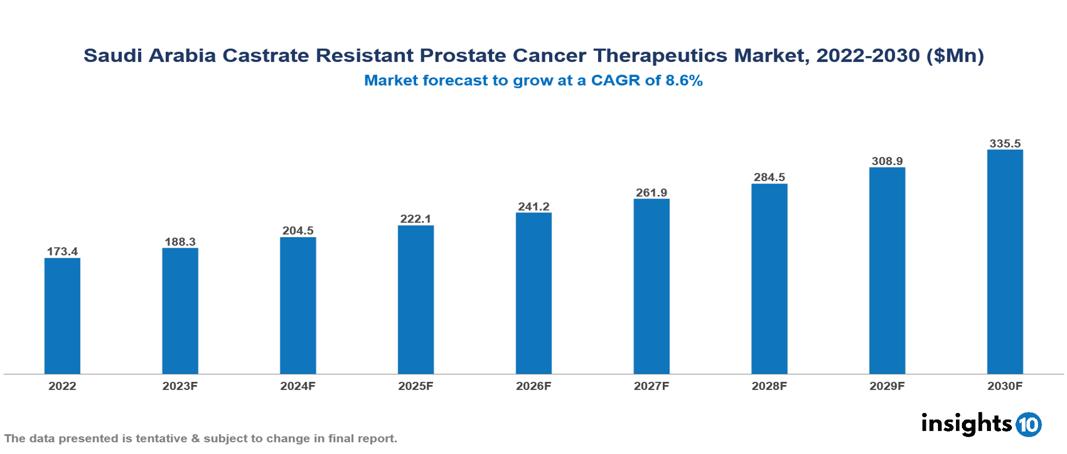

Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market valued at $173 Mn in 2022, projected to reach $335 Mn by 2030 with a 8.6% CAGR. In conclusion, the rising incidence of prostate cancer and the aging demographic, along with the confluence of a proactive and informed patient population, alongside a burgeoning focus on personalized medicine in Saudi Arabia underscore the critical need for advancements in Castrate Resistant Prostate Cancer treatment. The Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market encompasses various players across different segments, including Pfizer, Johnson & Johnson, Sanofi, Bayer, Roche, Tabuk Pharmaceutical, Julphar, Novartis, AstraZeneca, Jamjoom Pharma, etc, among various others.

Buy Now

Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market Analysis Executive Summary

Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market valued at $173 Mn in 2022, projected to reach $335 Mn by 2030 with a 8.6% CAGR.

Castration-resistant prostate cancer (CRPC) is a kind of prostate cancer that progresses despite testosterone level reduction, which is commonly done by surgical or medicinal castration. Lowering testosterone levels can impede the development of prostate cancer cells, which frequently rely on the male hormone testosterone for growth. Prostate cancer can, however, occasionally develop resistance to this hormone treatment. Chemotherapy, immunotherapy, and targeted medicines are available as CRPC treatments. Drugs used in chemotherapy, such as cabazitaxel or docetaxel, can be used to halt the growth of cancer. Immunotherapies, such as spuleucel-T, elicit an immune response that targets cancerous cells. Targeted treatments, like abiraterone or enzalutamide, concentrate on particular pathways that contribute to the development of cancer. To control colorectal cancer and enhance quality of life, individualized treatment regimens are created depending on variables such as cancer stage and patient health.

Prostate cancer ranks as the sixth most common kind of cancer in Saudi Arabia. It is quite common, and most cases are either metastatic or detected at an advanced stage of the disease. Within five years of their original diagnosis, 10–20% of men with prostate cancer are likely to develop CRPC. The rising incidence of prostate cancer and the aging demographic, along with the confluence of a proactive and informed patient population, alongside a burgeoning focus on personalized medicine in Saudi Arabia underscore the critical need for advancements in Castrate Resistant Prostate Cancer treatment.

Pfizer is presently in the lead, with Johnson & Johnson and Sanofi following suit, according to the revenue made by each company's CRPC therapy portfolio. With more innovative strategies like olaparib and darolutamide, respectively, certain corporations, including Bayer and AstraZeneca, are pushing the envelope. These medications focus on certain CRPC pathways and might play important roles in the future.

Market Dynamics

Market Growth Drivers

Increasing Prevalence: Prostate cancer has emerged as the most prevalent cancer among men in Saudi Arabia, a trend exacerbated by a consistent rise in its incidence. The growing number of affected individuals intensifies the urgency for innovative and efficacious treatment modalities. The escalating burden of CRPC in the country is further compounded by an aging population. As individuals age, the risk of developing prostate cancer increases, contributing to the expanding demographic affected by CRPC.

Increasing Public Awareness: Concurrently, there is a notable surge in public awareness campaigns and the influence of patient advocacy groups. These initiatives empower individuals to actively seek superior treatment options and participate in clinical trials, fostering a culture of patient engagement and informed decision-making. This heightened awareness propels the demand for personalized and evidence-based therapies, reflecting a paradigm shift in the patient's role in healthcare.

Increasing need for Personalised Medicine: A pivotal factor in addressing the complexities of CRPC is the evolving landscape of personalized medicine and targeted therapies. Recognizing the inherent heterogeneity of castrate-resistant prostate cancer, researchers are increasingly focusing on developing therapies tailored to specific genetic mutations or molecular pathways within individual patients. This precision medicine approach holds immense promise for optimizing treatment outcomes by directly targeting the unique characteristics of each patient's cancer.

Market Restraints

High treatment costs: Novel CRPC treatments tend to be expensive, making them unaffordable for many patients, especially those with little financial resources or those who depend on public insurance. The strain from this heavy economic burden also affects healthcare finances, which restricts the therapies' broader acceptance and accessibility.

Lack of qualified healthcare personnel: A lack of doctors with the necessary training in handling CRPC, such as urologists and oncologists, might make it more difficult to diagnose patients and arrange their treatments. To reduce this disparity, funding for healthcare workforce development and recruiting qualified workers to neglected regions are essential.

Limited data and research infrastructure: In the Saudi setting, comprehensive data-gathering methods and empirical research are necessary to comprehend the efficacy and safety of novel therapeutic interventions. The local research initiatives and the successful modification of treatment procedures to the unique requirements of the Saudi population may be impeded by deficiencies in data infrastructure and research funding.

Healthcare Policies and Regulatory Landscape

The Ministry of Health oversees healthcare policies in Saudi Arabia, aiming to provide quality treatment universally. This involves investing in infrastructure, increasing insurance coverage, and promoting preventive measures. To ensure this goal is met, the Saudi Food and Drug Authority (SFDA) plays a crucial role. The SFDA, the sole agency regulating drugs, meticulously assesses the safety, efficacy, and quality of medications and medical equipment before their market release. This instills confidence in the healthcare system, safeguarding public health. Additionally, the SFDA rigorously monitors the production, marketing, and distribution of pharmaceuticals to prevent the sale of counterfeit products and maintain ethical business practices. Through its stringent framework and international collaborations, the SFDA significantly contributes to Saudi Arabia's healthcare objectives, establishing a solid foundation for a secure and healthy population.

Competitive Landscape

Key Players:

- Pfizer

- Johnson & Johnson

- Sanofi

- Bayer

- Roche

- Tabuk Pharmaceutical

- Julphar

- Novartis

- AstraZeneca

- Jamjoom Pharma

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Saudi Arabia Castrate Resistant Prostate Cancer Therapeutics Market Segmentation

By Route

- Parenteral Route

- Oral Route

- Others

By Therapy

- Hormone Therapy

- Chemotherapy

- Immunotherapy

- Radiotherapy

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

By End User

- Hospitals

- Specialty Clinics

- Homecare

- Academics & Research Centers

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

France Burn Ointment Market Analysis

Pharmaceuticals

Japan T-Cell Lymphoma Market Analysis

Pharmaceuticals

France Dry Eye Medication Market Analysis

Related reports (by geography)

Pharmaceuticals

Saudi Arabia Varicella Vaccine Market Analysis

Pharmaceuticals

Saudi Arabia Cell Based Immunotherapy Market Analysis

Pharmaceuticals

Saudi Arabia Hypersomnia Therapeutics Market Analysis

Pharmaceuticals