Healthcare Services

Mexico Healthcare Insurance Market Analysis

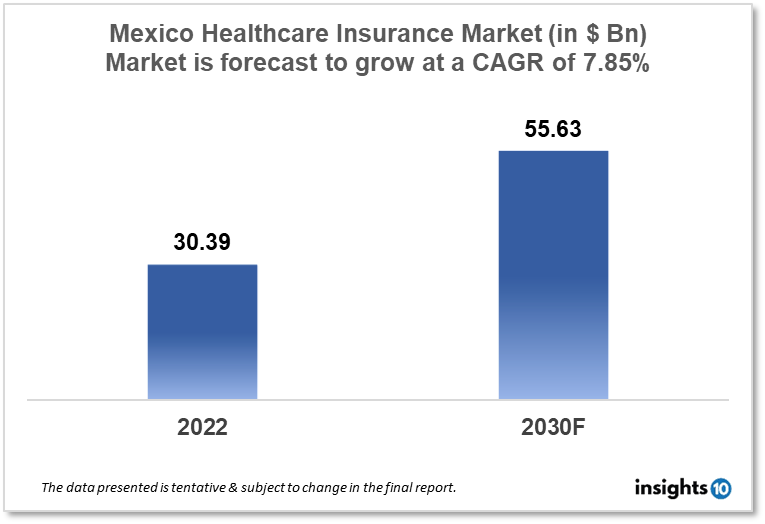

The Mexico healthcare insurance market is projected to grow from $30.39 Bn in 2022 to $55.63 Bn by 2030, registering a CAGR of 7.85% during the forecast period of 2022 - 2030. The main factors driving the growth would be the growing demand for healthcare services, regulatory changes, increasing affordability and technological advancements. The market is segmented by component, provider, coverage, by health insurance plans and end-user. Some of the major players include Grupo Nacional Provincial, Grupo Financiero Banorte, AXA, Metlife and Allianz.

Buy Now

Mexico Healthcare Insurance Market Executive Summary

The Mexico healthcare insurance market is projected to grow from $30.39 Bn in 2022 to $55.63 Bn by 2030, registering a CAGR of 7.85% during the forecast period of 2022 - 2030. Mexico spent 5.43% of GDP, or $540 per person, on national health expenses in 2019, up from 5.38% of GDP or $521 per person in 2018.

Mexico has a dual-sector healthcare system, meaning that both the public and private sectors provide medical care. While the commercial sector serves those who can afford to pay for healthcare services or have private insurance, the public sector is in charge of delivering healthcare services to the population without access to private insurance.

The healthcare insurance market in Mexico is governed by the Mexican Social Security Institute (IMSS) and the National Health Insurance Commission (Seguro Popular). While Seguro Popular takes care of the uninsured, IMSS is in charge of delivering healthcare services to the formal sector of the economy, which includes workers and their families. In Mexico, there are numerous private health insurance firms that offer healthcare insurance to individuals and families in addition to the public sector. These businesses provide a range of healthcare insurance policies, including entry-level ones that only cover hospitalisation and emergency treatment and more comprehensive ones that include cover prescription medications, dental work, and maternity care.

Market Dynamics

Market Growth Drivers

The Mexico healthcare Insurance market is expected to be driven by factors such as:

- Rise in demand for healthcare services- The demand for healthcare services is growing in Mexico as a result of both the country's growing elderly population and general population growth. This provides a wide base for the market for the healthcare insurance market, which is anticipated to develop as more people turn to insurance coverage to assist them in covering their medical costs

- Regulatory changes- The government of Mexico has passed a series of legislative changes that have helped the country's market for health insurance to grow. For instance, as a result of the General Health Law's passing, more insurance providers now provide health insurance coverage in the country

- Increasing affordability- The government of Mexico has made several policies over the last decade to enhance the cost-effectiveness of insurance and healthcare services. These policies have made it easier for more individuals to get access to healthcare services and insurance

- Technological advancements- It has been simpler for insurers to provide cutting-edge insurance products and services because of digital health platforms and other technology developments in the healthcare industry. This has contributed to the growth of the medical insurance market

Market Restraints

The following factors are expected to limit the growth of the healthcare insurance market in Mexico:

- High levels of informality- Since there is a sizable informal sector in Mexico, many people do not have formal jobs and cannot obtain health insurance through their employers. This limits the potential market for healthcare health insurers

- Economic instability- The recent economic volatility in Mexico has the potential to affect the market for health insurance. People are less likely to purchase insurance in times of economic hardships which will limit the demand for insurance products

- Limited coverage- Despite attempts to improve access to healthcare services, there are still wide differences in coverage among urban and rural areas, as well as between individuals with various incomes. This restricts the potential market for health insurance providers because many people might not see the point in getting insurance if they can't access medical care locally

Competitive Landscape

Key Players

- Grupo Nacional Provincial (MEX)- GNP is one of Mexico's biggest single insurance companies. GNP holds a large market share in various areas including basic insurance, car insurance, life insurance, home insurance, business insurance and medical insurance. GNP is owned by Grupo Bal, a privately held group of Mexican companies. In 1992, "Grupo Bal" acquired "La Nacional Compañía de Seguros", and "Seguros la Provincial". The name was changed to "Grupo Nacional Provincial" after the merger

- Grupo Financiero Banorte (MEX)- It provides insurance protection for risks like life, home, auto, integral protection, personal injury, and property damage to businesses. Additionally, it provides services like payroll, remittance, estate planning, collection, trust, financing, leasing, factoring, foreign exchange, asset management, foreign trade, internet banking, mobile banking, and international banking

- AXA- AXA Seguros, a division of the international insurance giant AXA, provides a variety of health insurance plans in Mexico. They provide protection against hospitalisation, medical costs, and other things

- Metlife- The MetLife firms have 153 years of experience and are a renowned global leader in protection planning, retirement and savings products, as well as a pioneering innovation. The MetLife firms provide retirement and savings products, life, accident, and health insurance through agents, direct marketing channels, and third-party distributors like banks and brokers

- Allianz- It offers products and services related to insurance. The company provides insurance for business, credit, engineering, major medical, life, home, liability, fire, transportation, and education. In Mexico, Allianz Mexico offers a global brand, business techniques, and a variety of services

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Healthcare Insurance Market Segmentation

By Provider (Revenue, USD Billion):

It mainly includes healthcare insurance that provides safety against the increasing cost of medical treatments and in case of health emergencies such as critical illnesses. Hence, it is the best way to safeguard medical expenses.

- Public

- Private

By Coverage Type (Revenue, USD Billion):

In terms of sales and market share, it is anticipated to rule the market over the projection period. This is explained by a number of benefits provided by life insurance, including guaranteed death payout and permanent coverage. Additionally, investing in these kinds of plans enables working professionals to save taxes

- Life Insurance

- Term Insurance

By Health Insurance Plans (Revenue, USD Billion):

- Health Maintenance Organization (HMO)

- Preferred Provider Organization (PPO)

- Exclusive Provider Organization (EPO)

- Point of Service (POS)

- High Deductible Health Plan (HDHP)

By Demographics (Revenue, USD Billion):

- Minors

- Adults

- Seniors

There is a high prevalence of lifestyle disease in the adult population that can increase health risks in the future. The population is more prone to cardiac and other diseases that require hospitalization. Healthcare insurance plans for seniors are more of a necessity, especially in the case of retirement. Also, it carries various advantages such as no medical screening before buying plans, includes coverage of the outpatient department, and provides the benefit of fee annual checkups along with lifetime renewability.

By End-user (Revenue, USD Billion):

- Individuals

- ?Corporates

A large number of people buy individual health plans as they are also customizable. Also, it gives more control over deductibles, co-pays, and benefits limits and is not dependent on employment status.

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Spain Soft Tissue Repair Market Analysis

Healthcare Services

Middle East Home Healthcare Market Analysis

Healthcare Services

UAE Antimicrobial Susceptibility Testing Market Analysis

Related reports (by geography)

Pharmaceuticals

Mexico Acne Drugs Market Analysis

Healthcare Services

Mexico Radiology Service Market Analysis

Medical Devices

Mexico 3D Printing Medical Devices Market Analysis

Pharmaceuticals