Medical Devices

Kenya Diabetes Devices Market Analysis

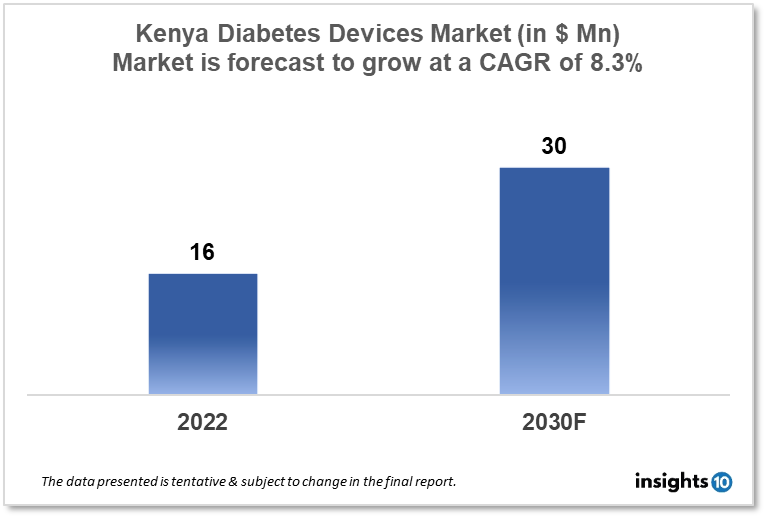

Kenya's Diabetes Devices Market is expected to witness growth from $16 Mn in 2022 to $30 Mn in 2030 with a CAGR of 8.30 % for the forecasted year 2022-2030. The main factors behind Kenya's increasing healthcare costs are the country's expanding population and the government's focus on improving healthcare facilities. This increased spending is likely to increase demand for diabetes devices. The market is segmented by type and by the end user. Some key players in this market include Kijenzi, APICALMED, Johnson & Johnson, Philipps Healthcare, Medtronic, Roche and Dexcom.

Buy Now

Kenya Diabetes Devices Healthcare Market Executive Analysis

Kenya's Diabetes Devices Market is expected to witness growth from $16 Mn in 2022 to $30 Mn in 2030 with a CAGR of 8.30 % for the forecasted year 2022-30. Kenya incurred costs for healthcare totalling $2,743 million. That is the same as 7% of the nation's GDP. Our ongoing medical expenses are paid for by families directly (32%), our government (31%), and our taxes (31%). Donor gifts come in second, with a sizable 26% share. In Kenya, health insurance makes up a pitiful 13% of total health spending.

In Kenya, 2.1% of adults (20-79 years) had diabetes in 2021. This equates to roughly 700,000 adult Kenyans who have diabetes. In Kenya, there were 1,600 fatalities brought on by diabetes in 2021. By 2045, the prevalence of diabetes in Kenya is expected to increase to 2.6%, representing an anticipated 1.3 million adult diabetics. Additionally, a sizable portion of diabetes cases in Kenya go undiagnosed; it is believed that 42.4% of adults with diabetes are unaware of their illness. This emphasises the significance of screening and early identification programmes to assist in identifying and managing diabetes in Kenya. People with diabetes in Kenya are able to benefit from and use diabetes devices in a variety of ways. They can assist people in better controlling their condition, lowering the chance of complications, and enhancing their general standard of life. The expense and availability of these devices, however, can restrict access, so initiatives to widen access to these devices and educational programs should take precedence.

Market Dynamics

Market Growth Drivers

The main factors behind Kenya's increasing healthcare costs are the country's expanding population and the government's focus on improving healthcare facilities. This increased spending is likely to increase demand for diabetes devices as more people become aware of how important it is to effectively manage their diabetes. Insulin pumps and continuous glucose monitoring systems are just a couple of the new and improved diabetes devices that manufacturers are continuously developing. Due to these technological developments, there will probably be a rise in the demand for diabetes devices in Kenya, particularly among those who want more cutting-edge and useful devices.

Market Restraints

In Kenya, many diabetes devices, including insulin pumps and continuous glucose monitoring systems, can be pricey, rendering them inaccessible to many Kenyans who might not be able to afford them. Because of their high price, these devices are in lower demand, which can restrain market development.

Competitive Landscape

Key Players

- Kijenzi (KE)

- APICALMED (KE)

- Johnson & Johnson

- DarioHealth

- Medtronic

- Philipps Healthcare

- Dexcom

Recent Notable Deals

2022: In order to improve diabetes care in Kenya, Sanofi Kenya, a pharmaceutical business, merged forces with Access Afya, a Kenyan healthcare organization, in 2022. In Kenya's underserved communities, the partnership seeks to offer affordable diabetes treatment, including diabetes devices and medications.

Healthcare Policies and Regulatory Landscape

The Pharmacy and Poisons Board (PPB), the Kenya Bureau of Standards (KEBS), and the Ministry of Health (MOH) are just a few of the government organisations that keep an eye on the healthcare laws and regulations in Kenya's market for diabetes devices. Diabetes devices must be registered with the PPB and are subject to Kenyan law. Before they can be sold in the nation, diabetes devices are required by the PPB to go through a rigorous registration procedure that includes testing, evaluation, and approval. Prior to going on sale to the general public, the registration procedure is meant to make sure that diabetes devices adhere to a set of safety and quality requirements. The creation and enforcement of guidelines for diabetes devices is the responsibility of the KEBS. Prior to being approved for use in Kenya, the KEBS guarantees that diabetes devices meet a number of requirements, including safety, quality, and performance standards. To make sure that producers of medical devices adhere to these standards, the KEBS also performs checks and audits.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Diabetes Devices Market Segmentation

By Type (Revenue, USD Billion):

The market is divided into blood glucose monitoring systems, insulin delivery systems, and mobile applications for managing diabetes within the type segment. Due to its convenience, ease of use, and usefulness in providing patients and healthcare professionals with real-time insights regarding diabetic conditions for integrated diabetes management, the segment for diabetes management mobile applications is anticipated to grow at the highest rate during the forecast period. Bare-metal Stents

- Blood glucose monitoring systems

- Self-monitoring blood glucose monitoring systems

- Continuous glucose monitoring systems

- Test strips/Test papers

- Lancets/Lancing Devices

- Insulin delivery Devices

- Insulin pumps

- Insulin pens

- Insulin syringes and needles

- Diabetes management mobile applications

By End User (Revenue, USD Billion):

The diabetes market is divided into hospitals & specialty clinics and self & home care, based on the end user.

- Hospitals & Specialty Clinics

- Self & Home Care

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

Indonesia Dental Endodontics Market Analysis

Medical Devices

South Africa Breastfeeding Accessories Market Analysis

Medical Devices

Africa Contraceptive Devices Market Analysis

Related reports (by geography)

OTC & Nutraceuticals

Kenya Herbal Supplements Market Report

Pharmaceuticals

Kenya NSCLC Drugs Market Analysis

Pharmaceuticals

Kenya PEGylated Proteins Market Analysis

Medical Devices