Medical Devices

Italy ENT Devices Market Analysis

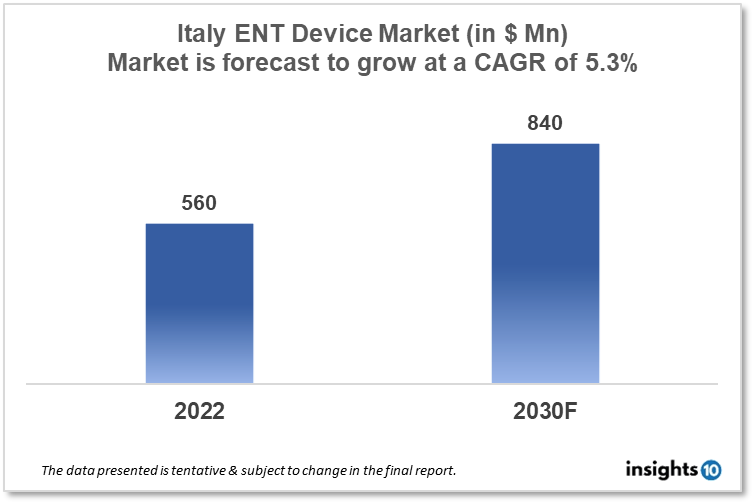

Italy's ENT Devices Market is projected to grow from $560 Mn in 2022 to $840 Mn by 2030, registering a CAGR of 5.3% during the forecast period of 2022-30. The rising prevalence of ENT disorders, such as hearing loss, sinusitis, and tonsillitis, is a major driver of the ENT device market. The market is highly competitive, with a large number of players operating in the space, ranging from small, specialized companies to large multinational corporations. The domestic key players in the Italy ENT devices market include Medtronic Italia, Grandi, and Moria.

Buy Now

Italy ENT Devices Market Analysis Summary

Italy's ENT Devices Market is projected to grow from $560 Mn in 2022 to $840 Mn by 2030, registering a CAGR of 5.3% during the forecast period of 2022-30.

Italy is a high-income, developed country located in Southern Europe comprising the boot-shaped Italian peninsula and several islands including Sicily and Sardinia. In Italy, various medical facilities and hospitals specialize in ENT treatment. Ospedale San Raffaele in Milan, Ospedale Pediatrico Bambino Gesù in Rome, and Ospedale Maggiore Policlinico in Milan are among them. The healthcare procurement system in Italy is divided into 33 procurement centers and a National Procurement Agency. The majority of purchases are made through public tender and are open to both domestic and foreign firms. Italy's government spends 9.6 % of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers Analysis

Italy is a mature market for medical equipment, ranking fourth in Europe behind Germany, France, and the United Kingdom, with over 4,500 companies (42 % distributors, 53 % makers, and 5 % service providers) and over 112,000 people. The manufacturing industry in Italy is comprised of a diverse network of small and micro firms, as well as start-ups. The rising prevalence of ENT diseases like hearing loss, tinnitus, and nasal congestion is driving up demand for ENT equipment in Italy. Demand for ENT devices is being driven by the development of new technology and gadgets, such as minimally invasive surgical techniques and digital hearing aids. These aspects could boost Italy's ENT Devices Market.

Market restrains.

Despite a sizable domestic manufacturing industry, Italy's domestic market for medical equipment is heavily reliant on imports. The Netherlands (26%) is the largest provider, followed by Germany (22%), Belgium (11%), France (9%), China (7%), and the United States (5%). The regulatory framework for medical devices in Italy, like in many other countries, is complex, and the clearance procedure for novel ENT devices can be lengthy and costly. New medical devices must be registered with the Italian Ministry of Health's Directorate General of Medical Devices and Pharmaceutical Services and have a unique identification number in the National Health System directory (Repertorio). These factors may deter new entrants into the Italy ENT Devices Market.

Competitive Landscape

Key Players

- Medtronic Italia- Based in Milan, Italy, this company produces a range of medical devices for use in ENT, including endoscopic instruments, surgical navigation systems, and balloon sinuplasty devices

- Grandi - Based in Turin, Italy, this company produces a range of ENT instruments, including ear specula, forceps, and suction tubes

- Bimar Medical - Based in Milan, Italy, this company produces a range of medical devices for use in ENT, including laryngoscopes, endoscopes, and video systems

- Moria- Based in Padua, Italy, this company produces a range of medical devices for use in ENT, including microkeratome systems, trephines, and surgical instruments

- 3B Scientific- Based in Turin, Italy, this company produces a range of medical training devices for ENT, including ear models, larynx models, and sinuses models

Healthcare Policies and Reimbursement Scenarios

In Italy, the regulation and reimbursement of ENT (Ear, Nose, and Throat) devices are overseen by various bodies, including the Italian Medicines Agency (AIFA) and the National Health Service (Servizio Sanitario Nazionale, or SSN). The AIFA is responsible for regulating medical devices in Italy, including ENT devices such as hearing aids, cochlear implants, and nasal dilators. The reimbursement of ENT devices in Italy is managed by the SSN. This system provides universal health coverage to all Italian citizens, and ENT devices are often covered under the insurance provision.

1. Executive Summary

1.1 Device Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Regulatory Landscape for Medical Device

1.6 Health Insurance Coverage in Country

1.7 Type of Medical Device

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

ENT Device Market Segmentation

The ENT Device Market is segmented as mentioned below:

By Product Type (Revenue, USD Billion):

- Diagnostic Devices

- Surgical Devices

- Hearing Aids

- Hearing Implants

- Co2 Lasers

- Image-Guided Surgery Systems

By Diagnostic Devices (Revenue, USD Billion):

- Endocsopes

- Hearing Screening Devices

By Surgical Device (Revenue, USD Billion):

- Powered Surgical Instruments

- Radiofrequency (RF) Handpieces

- Handheld Instruments

- Balloon Sinus Dilation Devices

- ENT Supplies

- Ear Tubes

- Voice Prosthesis Devices

By End Users (Revenue, USD Billion):

- Hospitals and Ambulatory Settings

- Home Use

- ENT Clinics

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Medical Devices

China Coronary Stents Market Analysis

Medical Devices

Denmark ECG Equipments Market Analysis

Medical Devices

Canada PET Scan Market Analysis

Related reports (by geography)

Healthcare Services

Italy Skilled Nursing Market Analysis

Digital Health

Italy 3D Imaging Market Analysis

Rare Diseases

Italy Phenylketonuria Therapeutics Market Analysis

Rare Diseases