Healthcare Services

Germany Cancer Pain Management Market Analysis

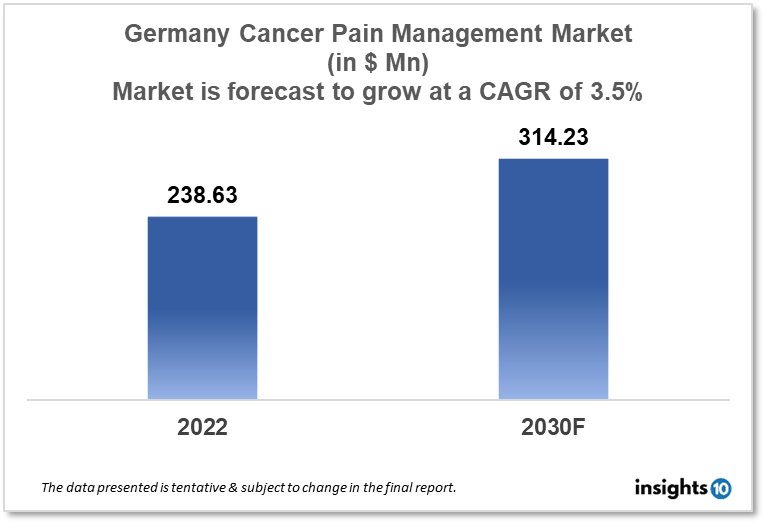

Germany's Cancer Pain Management market is projected to grow from $238.63 Mn in 2022 to $314.23 Mn by 2030, registering a CAGR of 3.5% during the forecast period of 2022 - 2030. The main factors driving the growth would be an increase in cancer cases and government initiatives. The market is segmented by drug type and by disease. Some of the major players include Grunenthal Pharma (DEU), Teva Pharmaceuticals, Pfizer, Abbott, and GW Pharma.

Buy Now

Germany Cancer Pain Management Market Executive Summary

Germany's Cancer Pain Management market is projected to grow from $238.63 Mn in 2022 to $314.23 Mn by 2030, registering a CAGR of 3.5% during the forecast period of 2022 - 2030. In 2019, Germany spent $4874.39 on healthcare per person, which was 28% more than the EU average of $3812. Furthermore, compared to other EU countries, Germany spends the highest percentage of its GDP (11.7%) on healthcare. As the majority of health spending in the EU is paid by public sources, just 12.7% of people in the country pay for their own healthcare, which is much less than the majority of other EU countries.

Cancer pain could be due to the disease itself or by treatments like surgery and chemotherapy. The selection and usage of medications are influenced by the kind, location, and intensity of pain experienced. A number of medications are used to relieve the pain brought on by cancer. For instance, it is advised to treat cancer pain that is mild to moderate with strong opioids rather than non-opioids such as acetaminophen and NSAIDs in cases of severe pain. Europe is a recognized player in the global market for the treatment of cancer pain, and it is also home to some of the leading pharmaceutical firms that are actively engaged in the creation of novel analgesics.

Market Dynamics

Market Growth Drivers

The World Health Organization reports that there are more cancer cases everywhere, including in Germany, where it is the leading cause of death. The need for efficient pain management therapies is being driven by this. Moreover, the development of specialized cancer pain clinics and the provision of financial assistance for cancer patients are some of the steps the German government has put in place to improve cancer care and pain management.

Competitive Landscape

Key Players

- Grunenthal Pharma (DEU)

- Teva Pharmaceuticals

- Pfizer

- Abbott

- GW Pharma

Notable Recent Deals

November 2022: Grunenthal Pharma entered into a joint venture with Kyowa Krin International for an established medicines portfolio. The Joint Venture Collaboration has a portfolio of 13 life-changing brands in six therapeutic categories, with the majority of its income coming from pain management medicines.

Healthcare Policies and Regulatory Landscape

The Federal Institute for Drugs and Medical Devices (BfArM), the Federal Joint Committee (G-BA), and the German Medical Association (BMA) oversee the regulatory and healthcare landscape in Germany for pain management. Treatments and drugs for pain management must adhere to the rules set forth by these organizations, including BfArM clearance and G-BA reimbursement through mandatory health insurance. The BMA also offers guidelines for doctors on moral and expert standards of care in pain management. These regulations seek to support the healthcare system's cost-effectiveness while ensuring that patients receive safe and efficient treatments.

Reimbursement Scenario

The Federal Joint Committee (G-BA), which is in charge of assessing and deciding the level of reimbursement for medical treatments and operations, sets the reimbursement scenario for pain management in Germany. Treatments must be declared medically essential and meet the G-BA requirement in order to be eligible for reimbursement. Medications and interventional procedures for pain management may be covered by statutory health insurance if the G-BA gives its approval. However, depending on the specifics of the case and the G-BA's judgment, some treatments might not be covered at all or might only be partially reimbursed. Patients can also choose private health insurance, which might offer more possibilities for covering pain management procedures.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Cancer Pain Management Market Segmentation

By Drug Type (Revenue, USD Billion):

Non-steroidal anti-inflammatory medicines relieve pain at the site of injury by blocking the cyclooxygenase enzyme, which prevents prostaglandin formation. NSAIDs are a class of medications that includes medications with analgesic, antipyretic, and, at higher doses, anti-inflammatory properties.

- Opioids

- Morphine

- Fentanyl

- Others

- Non-Opioids

- Acetaminophen

- Non-Steroidal Anti-Inflammatory Drugs (NSAIDs)

- Nerve Blockers

By Disease Indication (Revenue, USD Billion):

Based on disease Indication the market is segmented into:

- Lung Cancer

- Colorectal cancer

- Breast cancer

- Prostate cancer

- Blood cancer

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Morocco Women Health Diagnostic Market Analysis

Healthcare Services

Spain Corneal Implants Market Analysis

Healthcare Services

Spain Community Oncology service Market Analysis

Related reports (by geography)

Rare Diseases

Germany Huntington's Disease Drugs Market Analysis

Rare Diseases

Germany Anthrax Therapeutics Market Analysis

Healthcare Services