Pharmaceuticals

France HIV Drugs Market Analysis

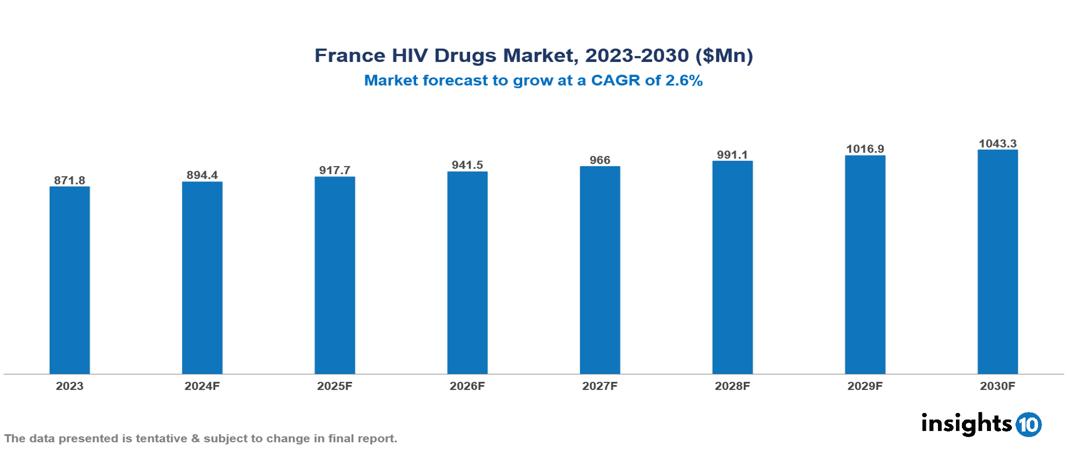

France HIV Drugs Market is at around $0.87 Bn in 2023 and is projected to reach $1.04 Bn in 2030, exhibiting a CAGR of 2.6% during the forecast period. The market is being influenced by factors such as increased HIV incidence, government initiatives, and technological improvements. The market is dominated by key players like Gilead Sciences, ViiV Healthcare, Boehringer Ingelheim International GmbH, Janssen Pharmaceuticals, Merck & Co., Bristol-Myers Squibb, AbbVie Inc., F. Hoffman-La Roche Ltd, Mylan, and Cipla.

Buy Now

France HIV Drugs Market Executive Summary

France HIV Drugs Market is at around $0.87 Bn in 2023 and is projected to reach $1.04 Bn in 2030, exhibiting a CAGR of 2.6% during the forecast period.

The HIV Drugs Market in France includes the manufacturing, distribution, and consumption of pharmaceuticals used to treat Human Immunodeficiency Virus (HIV) within the French healthcare system. To manage HIV infection and stop it from progressing to acquired immunodeficiency syndrome (AIDS), this market includes a variety of antiretroviral medicines, including combination therapies. The dynamics of this sector within the French healthcare environment are heavily influenced by factors like government regulations, healthcare infrastructure, and breakthroughs in drug research.

Antiretroviral treatments that address different phases of the disease are available in a wide variety on the French market for HIV therapies. Government initiatives, growing awareness, and improvements in treatment choices are driving the industry. The high expense of prescription drugs and obstacles to access for specific patient populations are drawbacks, though.

The global HIV medicine market has grown rapidly, with a value reaching $31.7 Bn in 2023. Rising HIV diagnoses, combined with government attempts to improve HIV management capabilities, have increased the HIV medicine sector. The market situation is shifting as generic competition increases. To continue forward, financial barriers must be removed, stigma minimized, and access to therapy expanded in underdeveloped countries.

Gilead has a considerable market share in France's HIV medicine market, believed to be approximately 25%. Biktarvy, their flagship medication, is France's best-selling HIV treatment, accounting for more than 15% of the market. Other Gilead HIV medications with a significant market presence include Genvoya, Descovy, and Atripla. Gilead's HIV medications are priced in France through government agreements and are routinely paid by the French healthcare system, making them affordable to the majority of patients.

Market Dynamics

Market Growth Drivers:

Increasing HIV prevalence: Despite advances in prevention and treatment, HIV continues to be a major public health concern in France. The rising number of HIV-positive people fuels the demand for HIV medications.

Government Initiatives: The French government may conduct a variety of initiatives to promote HIV treatment access, such as pharmaceutical subsidies or public awareness campaigns. These efforts can help to boost market growth by increasing the patient pool.

Technological Advancements: Continued research and development in the field of HIV treatment results in the release of new and more effective medications. Long-acting injectables and new antiretroviral treatments could drive market expansion.

Market Restraints:

Regulatory Hurdles: The regulatory process for authorizing new HIV medications in France can be stringent and time-consuming. Delays in obtaining regulatory approval or changes in regulatory standards may impede the introduction of innovative medicines to the market.

Generic Competition: The availability of generic HIV medications can lower prices and reduce market share for branded products. As patents expire and generics become more widely available, businesses may face increased competition and price pressure.

Stigma and Discrimination: The stigma and discrimination around HIV/ AIDS may discourage people from seeking testing, treatment, and care. This may reduce demand for HIV medications and impede efforts to restrict the virus's spread.

Healthcare Policies and Regulatory Landscape

The Agence nationale de sécurité du médicament and des produits de santé (ANSM) is a public body who report to the Ministry of Health. On behalf of the French government, it ensures the safety of health products and enables access to novel medicines. ANSM inspectors monitor compliance with relevant rules and regulations through audits and inspections, and they have the right to impose various enforcement measures. The process of centralized approvals in partnership with the European Medicines Agency (EMA) is more difficult, requiring compliance with both national and EU regulatory standards. The method for negotiating reimbursement after approval adds to the complexity of drug approval in France.

Competitive Landscape

Key Players:

- Gilead Sciences

- ViiV Healthcare

- Boehringer Ingelheim International GmbH

- Janssen Pharmaceuticals

- Merck & Co.

- Bristol-Myers Squibb

- AbbVie Inc.

- F. Hoffman-La Roche Ltd.

- Mylan

- Cipla

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

HIV Drugs Market Segmentation

By Drug Class

- Integrase Inhibitors

- Non- Nucleoside Reverse Transcriptase Inhibitors (NRTIs)

- Combination HIV Medicines

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Pharmaceuticals

Middle East Dermatology Drugs Market Analysis

Pharmaceuticals

Canada Cardiovascular Diseases Therapeutics Market Analysis

Related reports (by geography)

Pharmaceuticals

France Peptic Ulcer Drugs Market Analysis

Pharmaceuticals

France Lung Cancer Therapeutics Market Analysis

Medical Devices