Pharmaceuticals

China Oncology Therapeutics Market Analysis

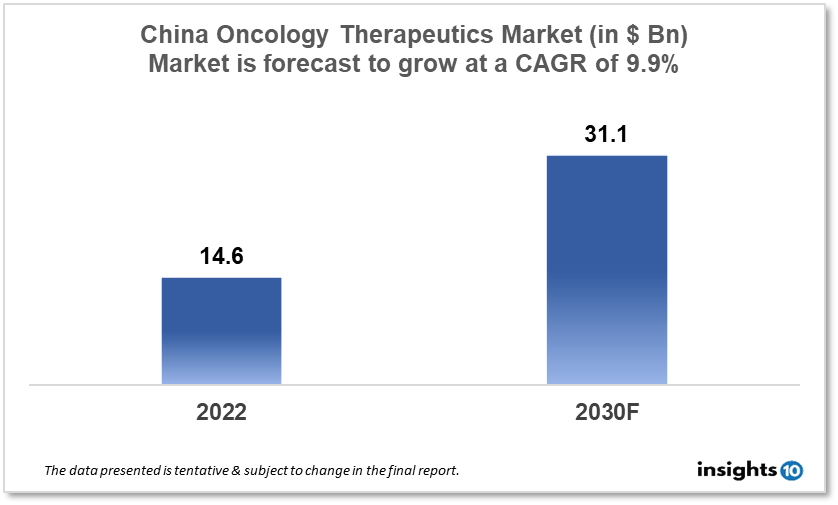

By 2030, it is anticipated that the China Oncology Therapeutics Market will reach a value of $31.1 Bn from $14.6 Bn in 2022, growing at a CAGR of 9.9% during 2022-2030. The Oncology Therapeutics Market in China is dominated by a few domestic pharmaceutical companies such as Bristol Myers Squibb, Boehringer Ingelheim, and CureVac. The Oncology Therapeutics Market in China is segmented into different types of cancer and different therapy type. The major risk factors associated with cancer are diet, alcohol, tobacco, air pollution, and physical inactivity. The demand for China Oncology Therapeutics is increasing on account of the rise in initiatives taken by the Government of the country.

Buy Now

China Oncology Therapeutics Market Analysis Summary

By 2030, it is anticipated that the China Oncology Therapeutics Market will reach a value of $31.1 Bn from $14.6 Bn in 2022, growing at a CAGR of 9.9% during 2022-2030.

China is an upper middle-income developing country in East Asia bordering the East China Sea, Korea Bay, and the South China Sea. Cancer is one of China's five high-priority illness areas, with patients suffering from severe health burdens and unmet demands, according to the Chinese government's Healthy China Action Plan (2019-2030). Patients from China account for over half of the global burden of gastric cancer, hepatocellular carcinoma, and oesophageal cancer.

Among the 393 assets under development by China's biopharmaceutical industry, 60% are focused on cancer kinds that rank first in terms of incidence rates: lung, colorectal, stomach, liver, and breast cancer. Local biotech firms are diversifying their immuno-oncology portfolios through a combination of in-house assets and partnerships. China's government spent 5.6 % of its GDP on healthcare in 2020.

Market Dynamics

Market Growth Drivers

China is a global leader in cell-therapy clinical trials, with a high level of activity. In China, 61 oncology novel active substances (NASs) were developed in the last five years, compared to just 41 from 2002 to 2016. This is most likely due to the National Medical Products Administration's (NMPA) regulatory expediting procedures, which aim to speed up the distribution of pharmaceuticals manufactured both locally and abroad to Chinese citizens.

Accelerating innovation in oncology in China is critical to progress in managing China's oncology burden and ensuring that patients receive improved, accessible, and equitable treatment options, all within the context of transformational ecosystem-shaping initiatives grounded in the local environment. Manufacturing is highly valued in China, whereas the services sector is expanding due to e-commerce trends. These aspects could boost China's Oncology Therapeutics Market.

Market Restraints

The number of oncologists per million people in China has climbed from 14 in 2005 to 26 in 2018, but there is still a long way to go before reaching the US benchmark of 60 oncologists per million people. For clinical practice, the local Chinese Society of Clinical Oncology Guidelines, which take drug accessibility and regional development differences into account, is strongly recommended. China is behind the US in terms of innovation, as assessed by the number of targets in the clinical stage of research. In the United States, clinical studies now span 550 targets, compared to 160 in China. These factors may deter new entrants into the China Oncology Therapeutics Market.

Competitive Landscape

Key Players

- BeiGene: BeiGene is a Chinese biopharmaceutical company that develops and produces a range of cancer therapeutics, including targeted therapies and immunotherapies. The company is currently developing several innovative cancer drugs, including ones that target solid tumours and hematologic malignancies

- Sinopharm Group: Sinopharm Group is a Chinese state-owned pharmaceutical company that produces a range of cancer therapeutics, including chemotherapy drugs, targeted therapies, and immunotherapies

- Hutchison China MediTech Limited (Chi-Med): Chi-Med is a Chinese biopharmaceutical company that focuses on the discovery and development of innovative cancer therapeutics

- Jiangsu Hengrui Medicine: Jiangsu Hengrui Medicine is a Chinese pharmaceutical company that specializes in the development and production of cancer therapeutics, including chemotherapy drugs and targeted therapies

Notable Recent Deals

March 2023: Calquence, a blood cancer medication developed by AstraZeneca, has received provisional clearance in China. The National Medical Products Administration (NMPA) of China has granted AstraZeneca's Calquence conditional approval to treat adult patients with mantle cell lymphoma (MCL) who have undergone at least one prior therapy. Calquence (acalabrutinib), a next-generation, selective Bruton's tyrosine kinase (BTK) inhibitor, was licenced for the first time in China, according to the British pharmaceutical giant. AstraZeneca stated that the drug's continued approval for this usage may be contingent on the results of ongoing randomised controlled confirmatory trials.

March 2023: Nubeqa (darolutamide), an oral androgen receptor inhibitor (ARi), has been licenced by the Chinese National Medical Products Administration (NMPA) in combination with docetaxel for the treatment of patients with metastatic hormone-sensitive prostate cancer. Nubeqa is already licenced in China for the treatment of non-metastatic castration-resistant prostate cancer patients who are at high risk of developing metastatic disease.

Healthcare Policies and Reimbursement Scenarios

The National Medical Medicines Administration (NMPA) is the regulatory authority in China responsible for the approval and regulation of therapeutic products, including cancer therapies. Furthermore, China has developed a specific programme known as the "National Reimbursement Drug List" (NRDL), which is a list of pharmaceuticals that are reimbursed under the national health insurance system.

1. Executive Summary

1.1 Disease Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Patient Journey

1.6 Health Insurance Coverage in Country

1.7 Active Pharmaceutical Ingredient (API)

1.8 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Epidemiology of Disease

2.2 Market Size (With Excel & Methodology)

2.3 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Diagnosis

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Oncology Therapeutics Segmentation

By Application (Revenue, USD Billion):

- Blood Cancer

- ?Colorectal Cancer

- Gastrointestinal Cancer

- Gynaecologic Cancer

- Breast Cancer

- Lung Cancer

- Prostate Cancer

- ?Others

By Drugs (Revenue, USD Billion):

- Revlimid

- Avastin

- Herceptin

- Rituxan

- Opdivo

- Gleevec

- Velcade

- Imbruvica

- Ibrance

- Zytiga

- Alimta

- Xtandi

- Tarceva

- Perjeta

- Temodar

- Others

By Therapy (Revenue, USD Billion):

- Chemotherapy

- Targeted Therapy

- Immunotherapy

- Hormonal Therapy

- Others

By Route of Administration (Revenue, USD Billion):

- Oral

- Parenteral

- Others

By Distribution Channel (Revenue, USD Billion):

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- ?Others

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

By 2030, it is anticipated that the China Oncology Therapeutics market will reach a value of $31.1 Bn from $14.6 Bn in 2022, growing at a CAGR of 9.9% during 2022-2030.

In China, the regulatory authority responsible for the approval and regulation of therapeutic products, including cancer therapeutics, is the Federal Institute for Drugs and Medical Devices (BfArM).

The Oncology Therapeutics Market in China is dominated by a few domestic pharmaceutical companies such as Bristol Myers Squibb, Boehringer Ingelheim, and CureVac.

Related reports (by category)

Pharmaceuticals

France Epigenetics Market Analysis

Pharmaceuticals

Kenya Plasma Protease C1-inhibitor Market Analysis

Pharmaceuticals

South Africa Dental Fluoride Treatment Market Analysis

Related reports (by geography)

Pharmaceuticals

China Interferons Market Analysis

Pharmaceuticals

China Gram Positive Bacterial Infections Market Analysis

Digital Health