Healthcare Services

Canada Robotic Surgery Services Market Analysis

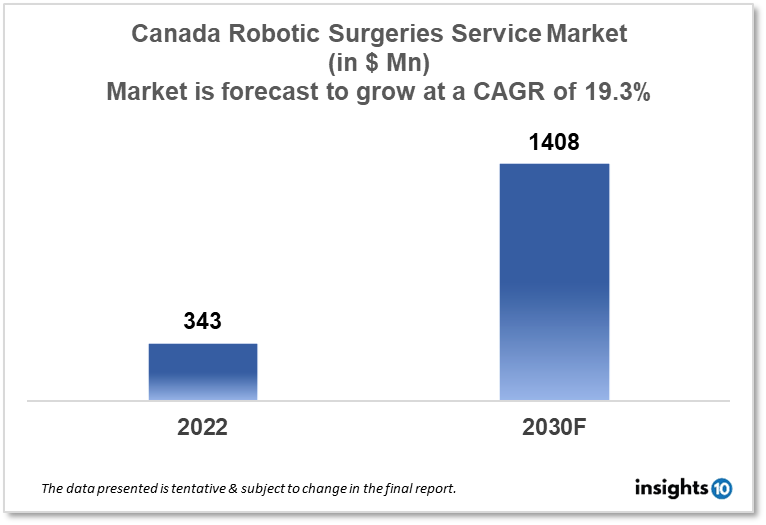

Canada's Robotic Surgery Service market size was valued at $343Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 19.30% % from 2022 to 2030 and will reach $1408 Bn in 2030. The robotic surgery service market will grow due to robotic surgery technology having made complex surgical procedures more accessible, especially in rural areas where access to specialized surgeons may be limited. The market is segmented by product and service type, application type, and end user. Some of the major players are Titan Medical Inc (CAN), HSS Global Technologies Inc (CAN), TransEnterix, Inc (CAN), and others.

Buy Now

Canada Robotic Surgery Service Market Executive Summary

Canada's Robotic Surgery Service market size was valued at $343Bn in 2022 and is estimated to expand at a compound annual growth rate (CAGR) of 19.30% % from 2022 to 2030 and will reach $1408 Bn in 2030. Healthcare spending in Canada is a significant part of the country's overall budget, and it has been steadily increasing over the years. According to the Canadian Institute for Health Information (CIHI), total healthcare spending in Canada reached $242.2 Bn in 2020. This amounts to approximately 11% of Canada's gross domestic product (GDP). The Canadian healthcare system is publicly funded, meaning that the government provides funding for most healthcare services through tax revenue. This funding is used to pay for services such as hospital care, physician services, and prescription drugs. Private insurance and out-of-pocket payments also contribute to healthcare spending in Canada, but the majority of funding comes from the government.

Healthcare spending in Canada has been growing at a faster rate than the economy as a whole, and this trend is expected to continue in the coming years. Factors such as an ageing population, increased demand for healthcare services, and the rising cost of new technologies and treatments are driving up healthcare costs in Canada.

Canada has a thriving healthcare sector and is making significant investments in the field of robotic surgery. The country has been a leader in the development and implementation of robotic surgical systems and has been at the forefront of adopting new technologies and techniques to improve patient outcomes and reduce the risks associated with surgery.

In recent years, Canada has seen increased adoption of robotic surgical systems, particularly in the fields of gynecologic, urologic, and colorectal surgery. There has been a growing interest in using these systems to perform minimally invasive procedures that can provide patients with improved outcomes, faster recovery times, and reduced pain and discomfort.

Canada has also been actively working to establish a robust regulatory framework for the use of surgical robots. The Canadian government has established guidelines for the use of these systems and is working to ensure that they are safe, effective, and accessible to patients.

Hence, Canada is considered to be at an advanced stage in the development and implementation of robotic surgery. The country is well-positioned to continue to be a leader in this field and is likely to continue to see significant growth and investment in the coming years.

Market Dynamics

Market Growth Drivers

In comparison to conventional surgical techniques, robotic surgery has been found to produce better surgical outcomes, with less blood loss, fewer problems, and quicker recovery times. Additionally, compared to conventional surgical techniques, robotic surgery provides greater precision and accuracy, enabling minimally invasive operations and lowering the risk of complications.

Furthermore, robotic surgery technology has facilitated the accessibility of complicated surgical operations, particularly in remote locations where access to specialised doctors may be constrained. Although robotic surgery equipment can have a hefty initial investment, many hospitals and healthcare facilities have discovered that over time, thanks to better patient outcomes and fewer complications, the technology can actually save money.

Market Restraints

The expense of purchasing and maintaining surgical robots may present a problem for some healthcare facilities, particularly smaller ones. Furthermore, without training and experience Due to a lack of skilled and knowledgeable doctors who are proficient in its application, robotic surgery technology may not be as widely available in other places.

Before robotic surgery becomes widely used, there may be legislative barriers that need to be cleared as well as difficulties in gaining funding for the treatments. Despite the advantages of robotic surgery, some patients and members of the public can be dubious or worried about the technology's efficacy and safety.

Competitive Landscape

Key Players

- Titan Medical Inc (CAN)

- HSS Global Technologies Inc (CAN)

- TransEnterix, Inc (CAN)

- Renishaw plc.

- Intuitive Surgical

- Medtronic

- THINK Surgical, Inc.

- Zimmer Biomet

Notable Deals

- In 2020, Intuitive Surgical Inc., the manufacturer of the da Vinci surgical system, acquired Medrobotics Corporation, a medical device company specializing in flexible robotic systems

- In 2019, Johnson & Johnson acquired Auris Health, a company that develops robotic technologies for use in minimally invasive procedures

Healthcare Policies and Regulatory Landscape

Policy changes and Reimbursement scenario

In Canada, the regulation of medical devices, including robotic surgical systems, is governed by Health Canada under the Medical Devices Regulations. Health Canada is responsible for evaluating and approving medical devices for use in Canada. The approval process includes a review of the device's safety, efficacy, and quality.

As for reimbursement, it varies by province. Each province has its own public health insurance plan and sets its own policies for covering the cost of medical procedures, including those performed with robotic surgical systems. Generally, the cost of a surgical procedure, including the use of a robotic surgical system, is covered by the public health insurance plan if the procedure is considered medically necessary. However, there may be some restrictions or limitations on coverage. Patients may also be responsible for paying a portion of the cost of the procedure, such as a co-payment or deductible.

1. Executive Summary

1.1 Service Overview

1.2 Global Scenario

1.3 Country Overview

1.4 Healthcare Scenario in Country

1.5 Healthcare Services Market in Country

1.6 Recent Developments in the Country

2. Market Size and Forecasting

2.1 Market Size (With Excel and Methodology)

2.2 Market Segmentation (Check all Segments in Segmentation Section)

3. Market Dynamics

3.1 Market Drivers

3.2 Market Restraints

4. Competitive Landscape

4.1 Major Market Share

4.2 Key Company Profile (Check all Companies in the Summary Section)

4.2.1 Company

4.2.1.1 Overview

4.2.1.2 Product Applications and Services

4.2.1.3 Recent Developments

4.2.1.4 Partnerships Ecosystem

4.2.1.5 Financials (Based on Availability)

5. Reimbursement Scenario

5.1 Reimbursement Regulation

5.2 Reimbursement Process for Services

5.3 Reimbursement Process for Treatment

6. Methodology and Scope

Robotic Surgery Services Market Segmentation

By Product and Services (Revenue, USD Billion):

The surgical robotics market volume data has been covered for all the major surgical robotics systems. In terms of value, the surgical systems market is anticipated to expand at a CAGR of 11.22% from 2018 to 2025.

- Instruments and Accessories

- Robotic Systems

- Services

By Application (Revenue, USD Billion):

Gynecology accounted for the largest market share in 2017 and is anticipated to expand at a CAGR of 7.0% from 2018 to 2025. This is explained by the rising prevalence of gynecological complications in women worldwide and the ongoing development of robotic technologies.

- General Surgery

- Gynecological Surgery

- Urological Surgery

- Neurosurgery

- Orthopedic Surgery

- Other Applications

By End User (Revenue, USD Billion):

The hospitals' segment had the largest market value in 2017 and experienced a CAGR of 13.20% from 2018 to 2025. However, during the projected period of 2018–2025, the ambulatory surgical center's income is predicted to rise at the highest CAGR of 18.20%.

- Hospitals

- Ambulatory Surgery Centers

Methodology for Database Creation

Our database offers a comprehensive list of healthcare centers, meticulously curated to provide detailed information on a wide range of specialties and services. It includes top-tier hospitals, clinics, and diagnostic facilities across 30 countries and 24 specialties, ensuring users can find the healthcare services they need.

Additionally, we provide a comprehensive list of Key Opinion Leaders (KOLs) based on your requirements. Our curated list captures various crucial aspects of the KOLs, offering more than just general information. Whether you're looking to boost brand awareness, drive engagement, or launch a new product, our extensive list of KOLs ensures you have the right experts by your side. Covering 30 countries and 36 specialties, our database guarantees access to the best KOLs in the healthcare industry, supporting strategic decisions and enhancing your initiatives.

How Do We Get It?

Our database is created and maintained through a combination of secondary and primary research methodologies.

1. Secondary Research

With many years of experience in the healthcare field, we have our own rich proprietary data from various past projects. This historical data serves as the foundation for our database. Our continuous process of gathering data involves:

- Analyzing historical proprietary data collected from multiple projects.

- Regularly updating our existing data sets with new findings and trends.

- Ensuring data consistency and accuracy through rigorous validation processes.

With extensive experience in the field, we have developed a proprietary GenAI-based technology that is uniquely tailored to our organization. This advanced technology enables us to scan a wide array of relevant information sources across the internet. Our data-gathering process includes:

- Searching through academic conferences, published research, citations, and social media platforms

- Collecting and compiling diverse data to build a comprehensive and detailed database

- Continuously updating our database with new information to ensure its relevance and accuracy

2. Primary Research

To complement and validate our secondary data, we engage in primary research through local tie-ups and partnerships. This process involves:

- Collaborating with local healthcare providers, hospitals, and clinics to gather real-time data.

- Conducting surveys, interviews, and field studies to collect fresh data directly from the source.

- Continuously refreshing our database to ensure that the information remains current and reliable.

- Validating secondary data through cross-referencing with primary data to ensure accuracy and relevance.

Combining Secondary and Primary Research

By integrating both secondary and primary research methodologies, we ensure that our database is comprehensive, accurate, and up-to-date. The combined process involves:

- Merging historical data from secondary research with real-time data from primary research.

- Conducting thorough data validation and cleansing to remove inconsistencies and errors.

- Organizing data into a structured format that is easily accessible and usable for various applications.

- Continuously monitoring and updating the database to reflect the latest developments and trends in the healthcare field.

Through this meticulous process, we create a final database tailored to each region and domain within the healthcare industry. This approach ensures that our clients receive reliable and relevant data, empowering them to make informed decisions and drive innovation in their respective fields.

To request a free sample copy of this report, please complete the form below.

We value your inquiry and offer free customization with every report to fulfil your exact research needs.

Related reports (by category)

Healthcare Services

Canada Stem Cell/Cord Blood Banking Market Analysis

Healthcare Services

Sweden Healthcare Reimbursement Market Analysis

Healthcare Services

Egypt Point Of Care (PoC) Molecular Diagnostic Market Analysis

Related reports (by geography)

Rare Diseases

Canada Phenylketonuria Therapeutics Market Analysis

Pharmaceuticals

Canada Migraine Drugs Market Analysis

Pharmaceuticals